Fiscal metering impacts the entirety of the CCS value chain, and is critical for building trust and ensuring successful CO2 transactions between different parties.

Carbon accounting is vital to CCS growth

Carbon capture and storage (CCS) is a pivotal technology for meeting the long-term temperature goals of the Paris Agreement. The International Energy Agency (IEA)’s Sustainable Development Scenario (SDS) estimates the size of the trading market of CCS to grow to at least 5 gigaton per year (Gt/y) by 2050, a similar scale to the current global market of natural gas in weight.

Reaching these trading levels requires vast technological, financial, and regulatory efforts. Large-scale CCS projects (e.g. Longship in Norway, Porthos in the Netherlands, and Acorn CO₂ SAPLING in the UK) are currently being developed and will enter into operation from 2024. At least five others are expected to follow, including cross-border projects. By 2030, the currently developing projects are expected to capture, transport and store over 40 Mt CO₂/year.

In order to meet the IEA’s targets, an exponential increase of CCS business must be sustained. In this context, thorough carbon accounting is vital.

A high level of accuracy

Accurate and traceable CO₂ measurements are required for fiscal and operational purposes across the CCS value chain. Fiscal metering allows verification of compliance with the Emission Trading System (ETS), which is needed to sell Emission Unit Alliances (EUAs) and generate revenue, rather than returning them. Furthermore, fiscal metering generates confidence in trading and ensures compliance with regulations.

Currently, in Europe, the accuracy requirements are dictated by the European Commission’s Measuring instruments directive (MID) and the International Organisation of Legal Metrology’s Internal Recommendation on Dynamic measuring systems for liquids other than water (OIML R 117-1), which require that the whole liquid CO₂ measurement system and the metering unit should deviate in accuracy by no more than 1.5% and 1%, respectively.

However, these requisites could evolve towards increased accuracy demands, as various indicators show. The EU taxonomy report sets the threshold of CO₂ leaks during the transport process alone at 0.5%, which further challenges the meter accuracy provision within MID and OIML. The accuracy of fiscal meters for rich liquid CO₂ mixtures remains to be confirmed.

Incentives for accurate flow measurements

Other incentives for accurate flow measurements include reducing taxation, considered by many countries to be the largest incentive to reduce emissions, and the increasing price of CO₂, a natural market driver.

CO₂ taxes are only expected to increase in the years to come. This is the case not only in Europe, where heavy tax plans exist – e.g. Norway’s target is to reach 200 €/ton of CO₂ by 2030 – but also in America and Asia – e.g. Canada expects to reach 134 $/ton CO₂ by 2030, while China is introducing a cap-and-trade program for the first time.

The price of CO2 has also increased steeply in recent years, and is forecasted to remain above 70 €/ton in the foreseeable future. This implies that the value of measurement accuracy (per every 1%) will be at least 3750 M€/year with the expected CO2 trade volumes in 2050.

As such, measurement uncertainty across the CCS chain translates to significant financial exposure for both parties in the CO₂ custody transfer process, depending on how each party’s revenue is affected by the + or – error. Since fiscal metering directly impacts the allocation of revenue, rightful financial allocation is of particular relevance to multistakeholder and cross-border CCS projects. From our perspective, we can see that the implications are that the flow measurement market for CO₂ trade will grow alongside that of the CCS business.

Relevance of fiscal metering oversight

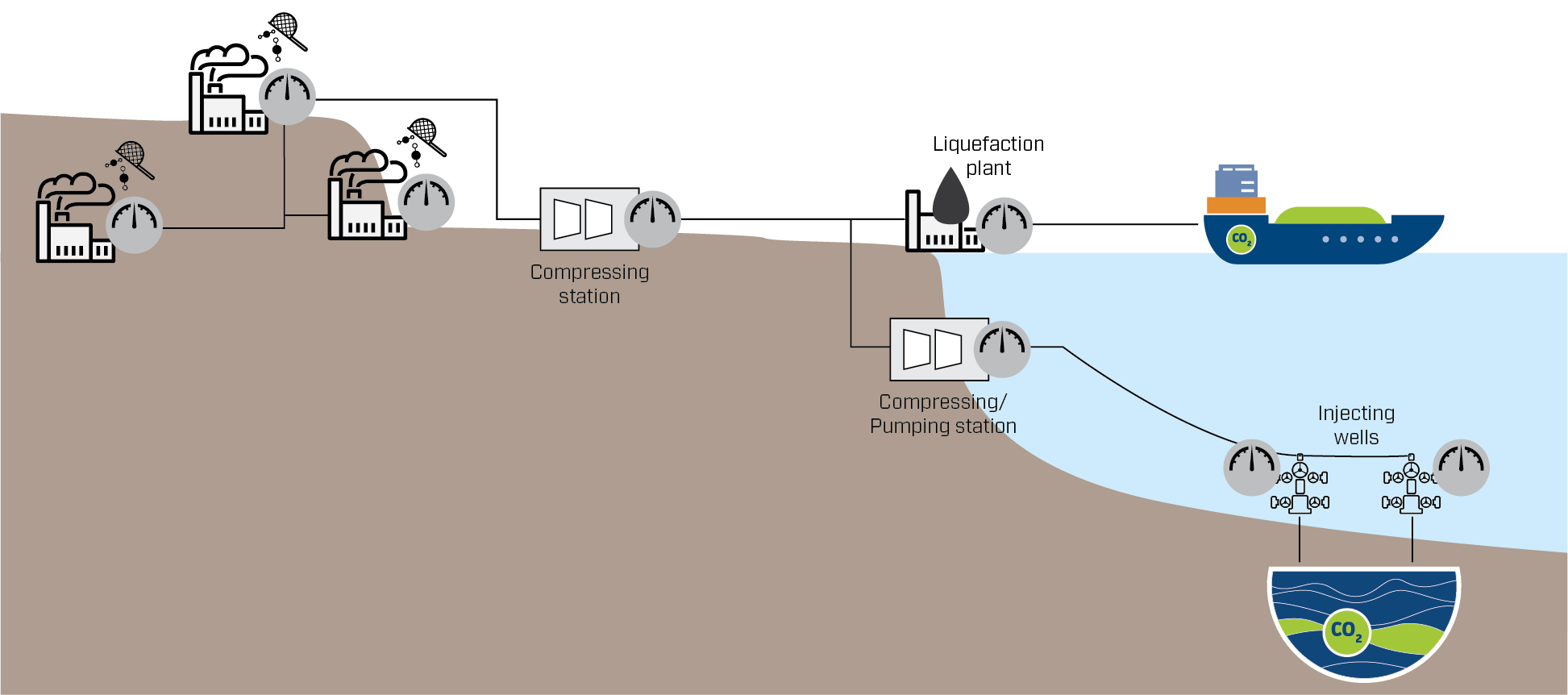

Fiscal metering is relevant for the entire CCS value chain. Whenever there is a custody transfer, or when required by regulations, fiscal metering nodes need to be established. Fiscal metering could be needed at a CO₂ capture and conditioning facility or at the entrance of transport networks, or in CO₂ terminals, pipeline exports, and injecting wells, etc.

An overview of accurate and traceable fiscal metering solutions is of the utmost relevance. The EU Emissions Trading System (ETS) allows emissions that are captured and stored in long-term geological storage sites to be subtracted. According to the current ETS regulation, the capture installation can only subtract the CO₂ from its reported emissions once it has been transferred to a pipeline transport network or to a storage site. This means that the capture installation would be fully responsible for the CO₂ emissions during ship/truck transport, which results in subtracted CO₂ emissions that are slightly lower than the amount of CO₂ captured.

However, the amendment to the ETS Directive (2003/87/EC), dated 14 July 2021, acknowledges ships and trucks as a means of transport. If it enters into force, it will imply that losses of CO₂ are the responsibility of the transport owner/operator, regardless of the means of transportation. This allows room for negotiations between the parties in order to account for CO₂ leakages and transportation emissions. This scenario emphasises the need for contractual agreements between the capture installation and the ship owner/operator, as well as accurate fiscal metering during on- and offloading of CO₂ and of CO₂ emissions from the ship propulsion system.

In transnational CCS projects, the applicable jurisdictions must also be considered. Under current provisions for CO₂ ship transport, each import/export party must submit a “Unilateral Declaration” to the International Maritime Organization (IMO). Bilateral agreements between the CO₂ exporting and importing countries should include provisions regarding cost sharing, monitoring of the transport, reporting, and liability in addition to permitting regimes.

CCS requires knowledge and trust

In sum, the realisation of CCS requires extensive metrology knowledge and technological innovations, as well as a deep understanding of the regulatory framework in order to swiftly ensure the transfer of liability, costs and risks, and build trust between operators along the value chain. The scientific community, operators, and policymakers must collaborate to navigate CCS towards the climate and societal objectives that the international community so urgently needs.

Find out more about our research:

TCCS-11: Enabling CCS via fiscal metering

CCUS Projects Networks: CO2 ship transport: Benefits for early movers and aspects to consider

PreemCCS: Legal and regulatory framework for Swedish/Norwegian CCS cooperation project report

Comments

Would it be possible to have this note in pdf formats?