Despite the several global crises of the last couple of years, environmental related risks are at the top of the list of global risks in a 10-years perspective. The World Economic Forum ranked Failing to mitigate climate change as the number one risk, followed by Failure to adapt to climate change, Natural disasters and extreme weather events, and Biodiversity loss and ecosystem collapse.

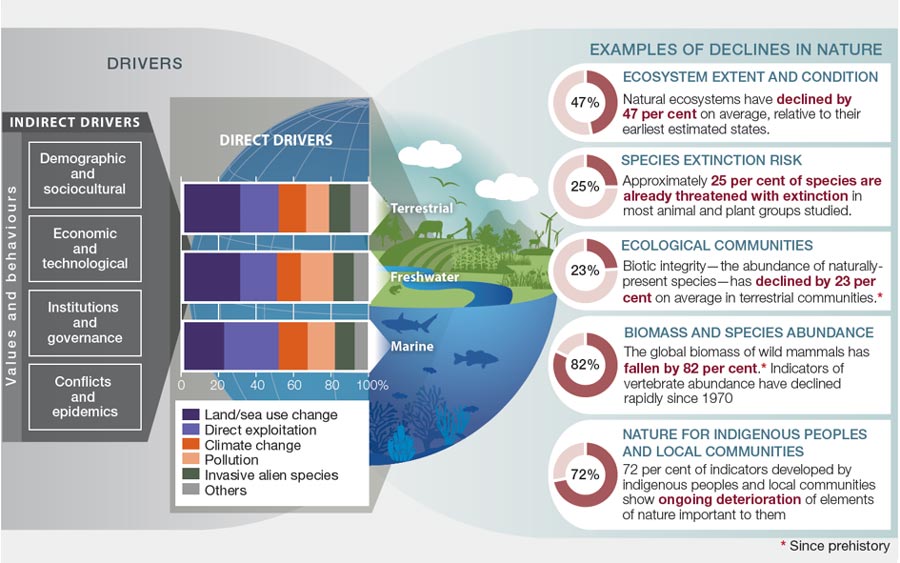

When thinking about the environment, climate change has been the main focus until recently. However, climate change is not the only environmental crisis of our times. A report by the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) highlighted that biodiversity and ecosystem services are deteriorating worldwide, and that the drivers of this change have accelerated over the last 50 years. They identified the main drivers of this loss to be changing use of land and sea, direct exploitation of natural resources, climate change, pollution, and the spread of invasive species. Most industries focus their efforts only on reducing climate change (through reduction of CO2 emissions) and on some types of pollution. In this context, systems for emission accounting and reporting are already in place for most of the industrial sectors. However, land use and direct exploitation are together responsible for over 50% of decline in nature, and there is currently no widespread system for assessing and monitoring these kinds of impacts.

Many separate initiatives are arising around the world

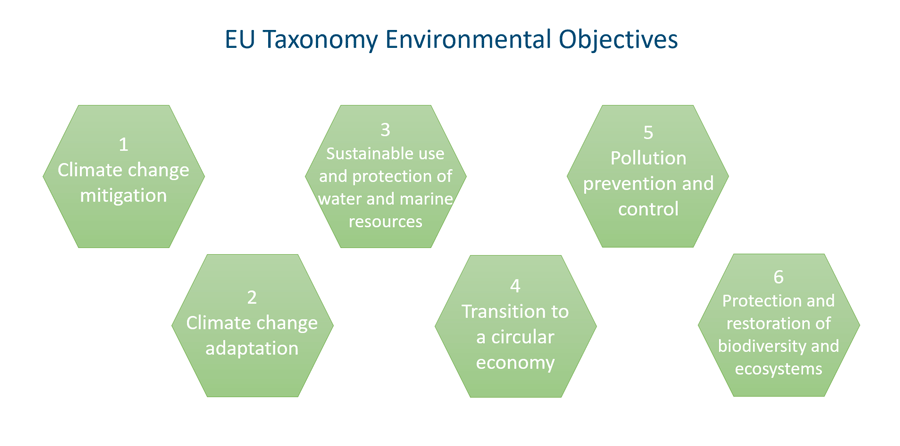

With the background we outlined, it is not surprising that when talking about sustainability, focus is becoming broader. The many separate initiatives arising on this topic worldwide are a sign of the importance and urgency of the matter. An example is given in the EU taxonomy, which has the key goal of redirecting capital flows towards sustainable investments. To do so, the taxonomy sets a framework to classify sustainable economic activities by defining six environmental objectives (as shown in the figure below). To be classified as sustainable, an activity needs not only to contribute to at least one of the 6 objectives, but must also not do significant harm to any of the remaining ones. While objectives 1 and 2 focus on climate change, objectives 3 and 6 consider protection and restoration of biodiversity, ecosystems and water and marine resources.

The SEEA Ecosystem Accounting

Another initiative is the SEEA Ecosystem accounting, which is a framework that has recently been developed to track changes in ecosystem extent and conditions, as well as to quantify their monetary value. The tool can be used to systematise the knowledge about natural systems and the services they provide, so that the costs of encroaching on nature can be taken into account as part of decision-making processes. The accounting has the aim of being geographically specific, so that it can also be developed at a local level (i.e., regional and municipal level). However, this tool is not specifically developed to be used for industrial activity or across industries.

Measuring industrial impacts on nature: a complex problem

The landscape of regulations, frameworks, and standards for nature-related sustainability is under rapid development, and there is currently no consensus in the scientific community on the best sets of indicators and metrics to measure and track impact. This is largely because drivers for deterioration of nature are multidimensional and ecosystems vary widely in the way they function, which introduces an added level of complexity and challenge when compared to climate change and its drivers. Indeed, if climate change has a single indicator (i.e. equivalent greenhouse gas emissions), impact on nature has no such single metric. The drivers for loss of biodiversity are multi-dimensional, which requires a set . No such set of indicators is currently established and agreed upon by the scientific community. The fact that there are several parallel initiatives partially overlapping trying to provide guidance on the same aspect adds a layer of complexity.

Parallel initiatives to help business track their impact on nature

The overarching global goals defined by the Global Biodiversity Framework (GBF) set the scene for action. The framework was signed at the United Nations Biodiversity Conference (COP15) in 2022 by 196 nations, which committed to achieving 4 overarching goals and 23 targets. Each country is also expected to prepare a national action plan on how to contribute to these goals, by the end of 2024. The first reporting to the UN on the achievement of these goals is expected to be in 2026. The action plans are also expected to address the industry’s role in achieving the goals, in particular in relation to Target 15, which states that businesses must be encouraged, through legal, administrative or policy measures, to monitor, assess and disclose their nature-related risks, dependencies, and impacts.

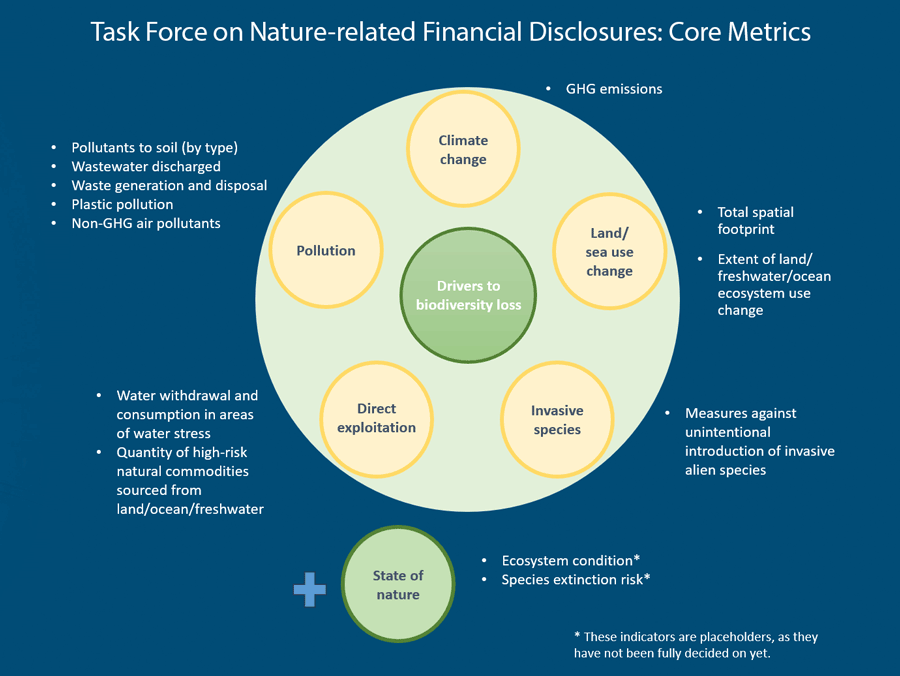

The Task Force on Nature-related Financial Disclosures (TNFD) is another global initiative that has introduced a framework for companies to evaluate and share details about key nature-related aspects. The TNFD defines 13 core metrics related to the main impact drivers and the state of nature (see the figure below). In addition, sector-specific indicators are also suggested. The number and the thematic spread of indicators give an idea on the complexity of the problem of quantifying impact on nature.

Biodiversity: Early compliance by industry has benefits

This is crucial to meet the 2030 targets. Due to the complexity of the topic, actors that start preparing early will have advantages. In Norway, Borregård is one of the early adopters of the reporting in line with the TNFD. A company’s transparency on nature-related impacts is also increasingly influencing on its public standing and funding possibilities. Finally, many sectors directly depend on nature-related goods and services, and must, to a greater extent, include nature-related impacts and dependencies in their risk management going forward.

Comments

No comments yet. Be the first to comment!